Having gained almost 16,000% for early shareholders, there’s little doubt that electric vehicle manufacturer Tesla (NASDAQ:TSLA) ranks among the most groundbreaking enterprises in business history. At the same time, much of its success has been attributed to the company scooping up the low-hanging fruit. Now under a more mature market environment and with competitors moving in, TSLA stock faces a more difficult road ahead.

To Tesla’s credit, while it didn’t exactly invent the EV, it pioneered the mobility platform’s integration into modern society. At the moment, the very idea of electric-powered transportation is practically synonymous with the company’s elegantly designed cars. However, the consumer base is not infinite. As the automotive industry taps out the wealthiest consumers, it must start addressing the middle-income crowd.

That’s where Tesla could end up stalling. And for that, I’m skeptical about TSLA stock.

Revenue Growth Concerns May Impact TSLA Stock

In the fourth quarter, Tesla posted revenue of $25.17 billion, up 3.5% against the year-ago period’s result. That brought total sales for 2023 to nearly $96.8 billion, a significant jump of almost 19% against 2022’s haul. Nevertheless, when the EV giant released its results in late January, the market wasn’t exactly thrilled.

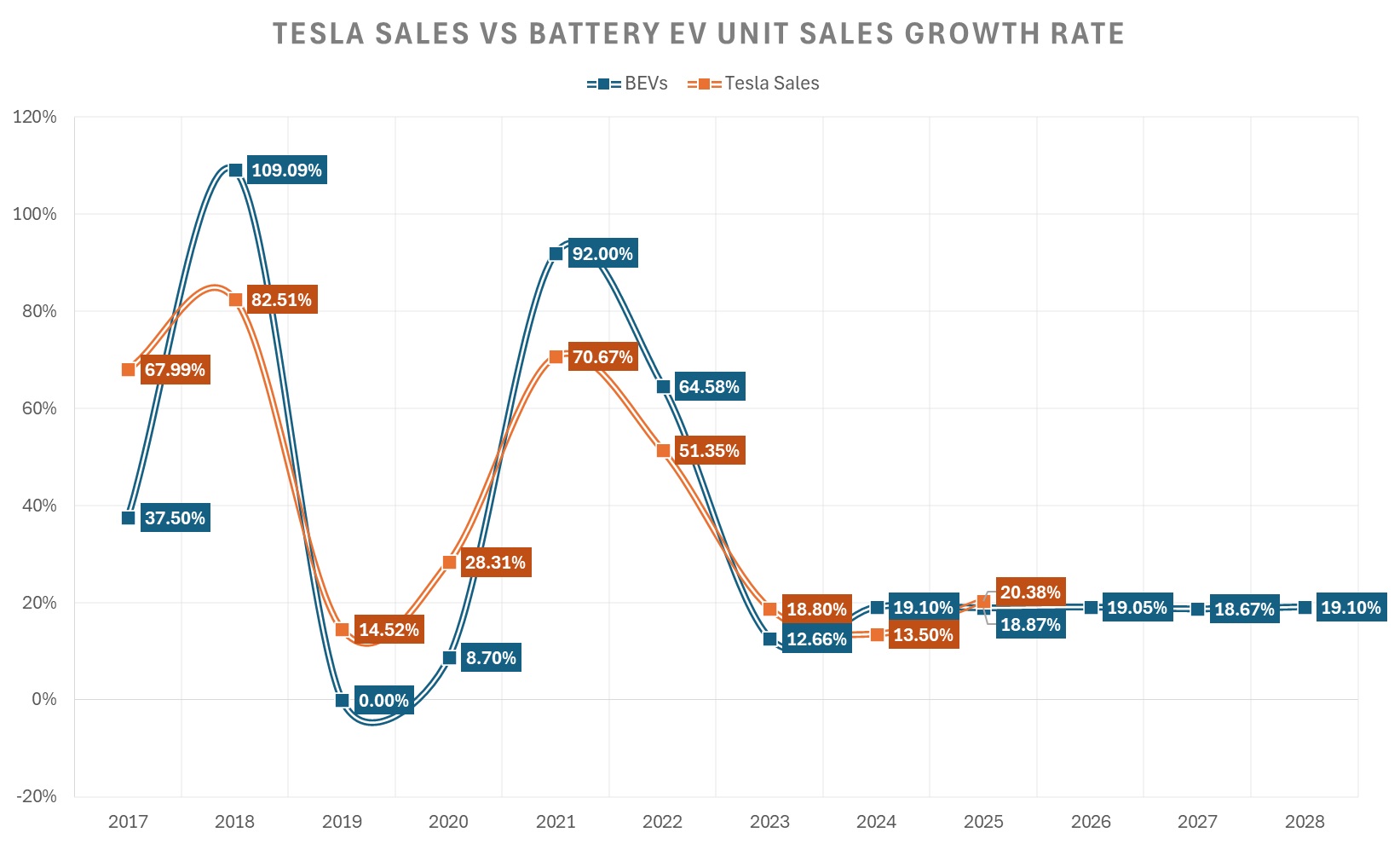

Among myriad concerns for the company – including earnings estimates for 2024 now slipping below 2023’s level – the fading sales growth struck me as particularly challenging. In the three years trailing the end of 2023, Tesla’s top line expanded at a compound annual growth rate (CAGR) of 21.63%. That might seem impressive on its own. However, U.S. battery EV (BEV) unit sales expanded at a CAGR of 22.85%.

In contrast, the framework was flipped between 2019 through 2021. Back then, Tesla’s top line expanded at a CAGR of 29.8%. For the domestic EV industry, unit sales saw a CAGR of 27.8%.

{kind=link}

In other words, Tesla can no longer expect to win by default. More competitors are moving in, from pure-play EV manufacturers to legacy automotive stalwarts making a pivot to electrification. That might not be a challenge that TSLA stock is suited for, presenting market risks.

Tesla May Have Run Out of Low-Hanging Fruit

Part of the reason for Tesla’s early success was the enthusiastic response from the consumer base. Similar to heightened demand for the latest Apple (NASDAQ:AAPL) products, the EV maker enjoyed a certain social cachet. Sure enough, Tesla took full advantage of the captivated audience.

However, consumers no longer see EVs as a novelty. Most impactful to TSLA stock is that the underlying enterprise can’t just do whatever it wants and expect people to show up on showroom floors with open wallets. As stated earlier, competition is rising – and rising across the entire price spectrum.

So, Tesla has to do more to pluck its fruits. It still can do so. However the problem is that the exercise consumes more energy, thus impacting metrics like profitability.

One of how Tesla has addressed the steadily maturing EV market has been to cut prices. For more than a year, the company started and fueled a sector-wide price war. While that hurts the competition, it’s also hurting Tesla.

Further, the disappointing performances by premium-level EV makers Rivian Automotive (NASDAQ:RIVN) and Lucid Group (NASDAQ:LCID) present major concerns for TSLA stock. The fallout suggests that the folks who wanted EVs already bought them.

Moving forward, the fight is only going to get tougher.

Auto Insurance: The Underappreciated Headwind

If you ever looked at auto insurance premiums this year and balked, you’re not alone. According to CBS News earlier this year, premiums around the nation have soared. Several factors are responsible for the spike, including lingering issues from the pandemic. Nowadays, vehicles are simply more expensive to replace thanks to inflation.

Further, a shortage of mechanics in the U.S. translates to longer wait times to fix vehicles. Unfortunately, this dynamic forces insurance companies to cover their clients during extended downtime, such as providing for rental cars.

Here, prospective EV drivers may believe they have a pass. However, insurance costs for electric cars typically command higher insurance rates than their combustion-powered counterparts. Why? Simply, EVs cost more. They also suffer damage more easily and are more expensive to repair.

With consumers already hurting from the aftershocks of Covid-19, paying a higher insurance bill isn’t exactly part of the game plan. And while Tesla drivers tend to be wealthier than average, the higher costs of everything are clearly affecting TSLA stock.

If they weren’t, why is Tesla slashing the prices of their vehicles?

On the date of publication, Josh Enomoto did not have (either directly or indirectly) any positions in the securities mentioned in this article. The opinions expressed in this article are those of the writer, subject to the InvestorPlace.com Publishing Guidelines.