Entering the public domain as a blank-check firm, Joby Aviation (NYSE:JOBY) – which specializes in electric vertical takeoff and landing (eVTOL) aircraft – received much fanfare early on. Unfortunately, as was the case with many other reverse mergers with special purpose acquisition companies (SPACs), the air taxi specialist suffered a severe drop in equity value. Nevertheless, as broader economic circumstances normalize, the JOBY stock outlook appears compelling.

Let’s summarize the main fundamental catalysts. First, eVTOLs generally align with the wider push for clean-emission transportation platforms. Second, as society grows, more people will take to the air, thus creating pollution – including noise pollution. Here, eVTOLs bring great promise to urban residents, offering a significantly quieter make sound profile than their combustion-powered counterparts.

For the JOBY stock outlook specifically, the underlying enterprise enjoys a partnership with Toyota (NYSE:TM), one of the world’s top automotive manufacturers. Not only that, Joby expanded its partnership with the auto giant with a long-term supply agreement.

So, despite the ugly stench around SPACs, the JOBY stock outlook appears positive. In fact, Wall Street analysts rate the underlying company as a consensus strong buy. Further, their average price target lands at $9.25, implying 56% upside potential.

Keep this target in mind because it’s very realistic, if not probable.

Rising Sentiment Backs Positive JOBY Stock Outlook

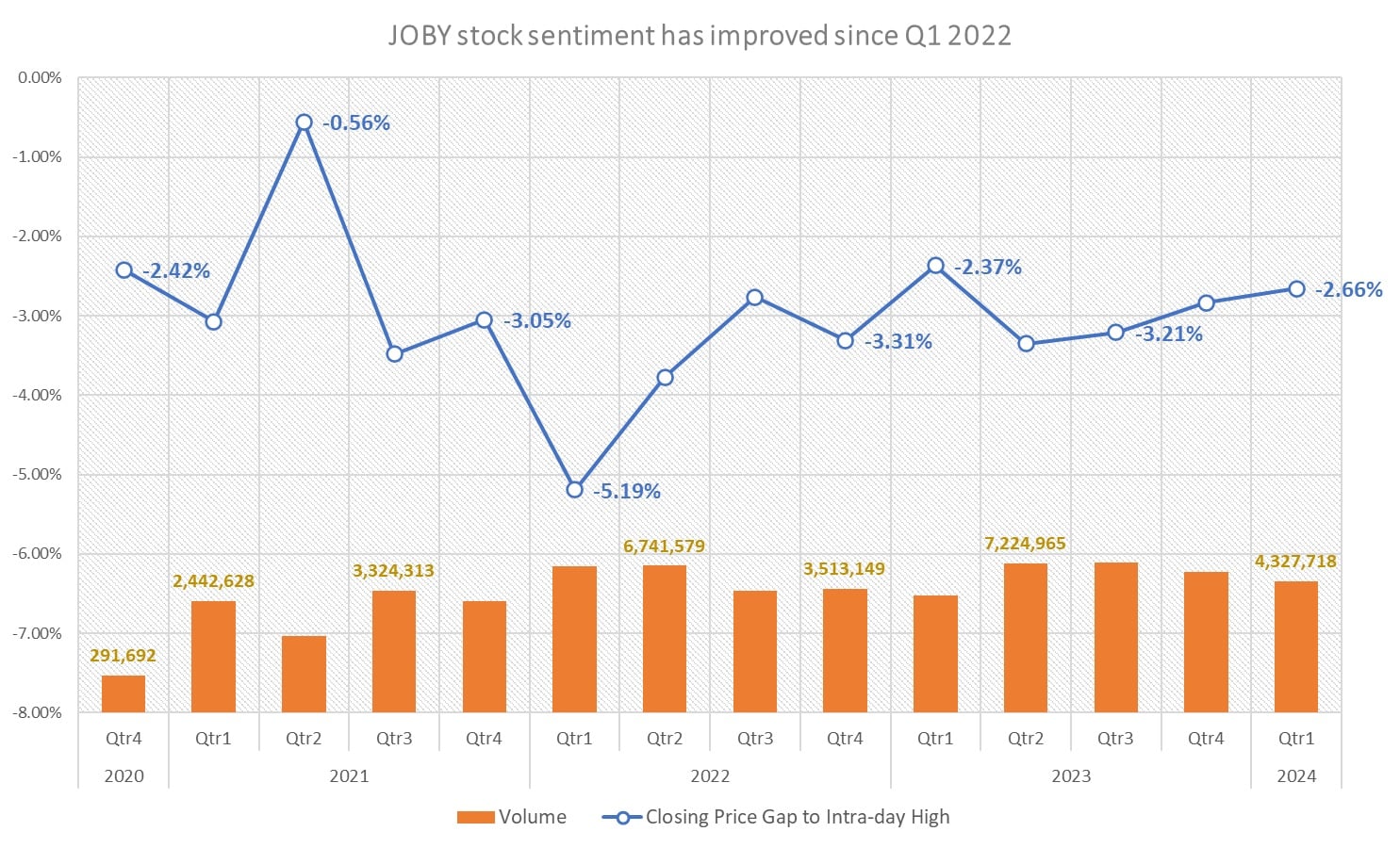

Obviously, in every trading session, there’s an intraday high, an intraday low and ultimately, a closing price. By logical deduction, if a security enjoys positive sentiment, its closing price on average should end closer to the intraday high as opposed to the low. Or, the average closing price should move steadily toward 0%. Essentially, that’s what we’re seeing with the eVTOL specialist, thus yielding an optimistic JOBY stock outlook.

{kind=link}

Back during the wild days of 2021, the average closing price was only off about half-a-percent from the intraday high (during the second quarter). However, as sentiment faded for Joby and most other SPAC-based initial public offerings (IPOs), this gap widened to 5.19% below parity in Q1 2022.

Nevertheless, from that quarter, sentiment for JOBY stock improved noticeably. Specifically, the gap between the average closing price to the intraday high was 3.35% in Q2 2023. By the time of writing, this metric narrowed to 2.66%.

Over the past 52 weeks, shares gained about 41%. This print aligns with the thesis of rising market sentiment, thus justifying an optimistic JOBY stock outlook.

The Shorts Could Get Blown Up

According to data from Fintel, JOBY incurs a short interest of 18.81% of its float. In addition, it also sees short interest ratio of 19.26 days to cover. Stated differently, if the bears wanted to unwind their entire short position, it would take about a month to do so based on average trading volume. However, signs already exist that the short traders could get blown up.

First, JOBY stock gained more than 7% in the business week ending Feb. 9. Something is driving bullish sentiment and part of the explanation could center on contrarian activities. Since bearish traders are contractually obligated to return their shares borrowed for the purpose of shorting, if the underlying security’s price rises, they would be forced to make good on the loan at a higher rate.

Obviously, from a shorting perspective, buying back borrowed shares at an elevated price would result in lost money. And if the security really goes bonkers, the bears could suffer catastrophic financial damage. Therefore, the smart pessimists recognize when the market moves against them early, thus mitigating the pain.

Still, when short interest and the underlying ratio to volume are excessively elevated, the dynamic could create a stampede effect – otherwise known as a short squeeze. A short squeeze appears to have panicked out Lucid Group (NASDAQ:LCID) bears last week, which was one of the reasons I was bullish on LCID.

I believe a similar dynamic could play out for Joby; hence, I’m very optimistic about the JOBY stock outlook.

Wall Street’s Giving You Free Money

Finally, no discussion about the bull case for the eVTOL manufacturer is complete without talking about the options market. Conspicuously, an unusual development occurred that arguably warrants a calculated risk.

In the options market, traders pay for everything. If you want time – that is, if you want an option that will expire far out into the future – you must pay a premium for that safety margin. If you want a cheaper option, then you must elect a contract that’s out the money (OTM) than in the money (ITM).

And if you do choose OTM options, the bid-ask spread tends to be wider. Mainly, that’s related to the level of activity for the option. Logically, OTM options are less predictable because it’s not clear whether they will end up as ITM contracts. Thus, the spread is wide as it’s difficult to find a buyer. Stated differently, a large gap exists between what the seller wants (ask) and what the buyer is willing to pay (bid).

However, in the case of the JOBY Jan 17 ’25 7.50 Call, the bid ($1.15)-ask ($1.20) spread as represented by the midpoint price ($1.17) comes out to only 4.27%. That’s lower than the JOBY Jan 17 ’25 5.50 Call, which features a spread of 8.2%.

I can’t emphasize this enough. In most circumstances, a cheaper option comes at the cost of a wider spread. Here, you’re getting a cheaper option with a narrower spread. If this dynamic holds up, you’re receiving a safety margin for free. And it’s a realistic target since the strike of $7.50 is inside that of the aforementioned $9.25 average price forecast.

The Takeaway: Free Money for a Compelling Speculation? Sign Me Up!

As with any investment, Joby Aviation carries risk. Because it was a former SPAC, big questions surround the enterprise’s forward viability. However, the eVTOL is a compelling market thanks to its myriad benefits. Therefore, many speculators are already incentivized to at least consider the opportunity.

However, if the Street is willing to give you a narrow spread for a cheap option, in my opinion, it’s worth taking the deal. It’s free money. So, if you want my takeaway regarding a JOBY stock outlook, here it is. If the spread remains this narrow when the market opens on Monday, I’m going in. Simple as that.

On the date of publication, Josh Enomoto did not have (either directly or indirectly) any positions in the securities mentioned in this article. However, the author intends to buy JOBY stock options if the specified conditions materialize. The opinions expressed in this article are those of the writer, subject to the InvestorPlace.com Publishing Guidelines.