[Editor’s note: “Buying Opendoor Today Could Be Like Buying Amazon in 1997” was previously published in June 2022. It has since been updated to include the most relevant information available.]

Anyone who follows me knows this: I’m super bullish on Opendoor (OPEN) stock.

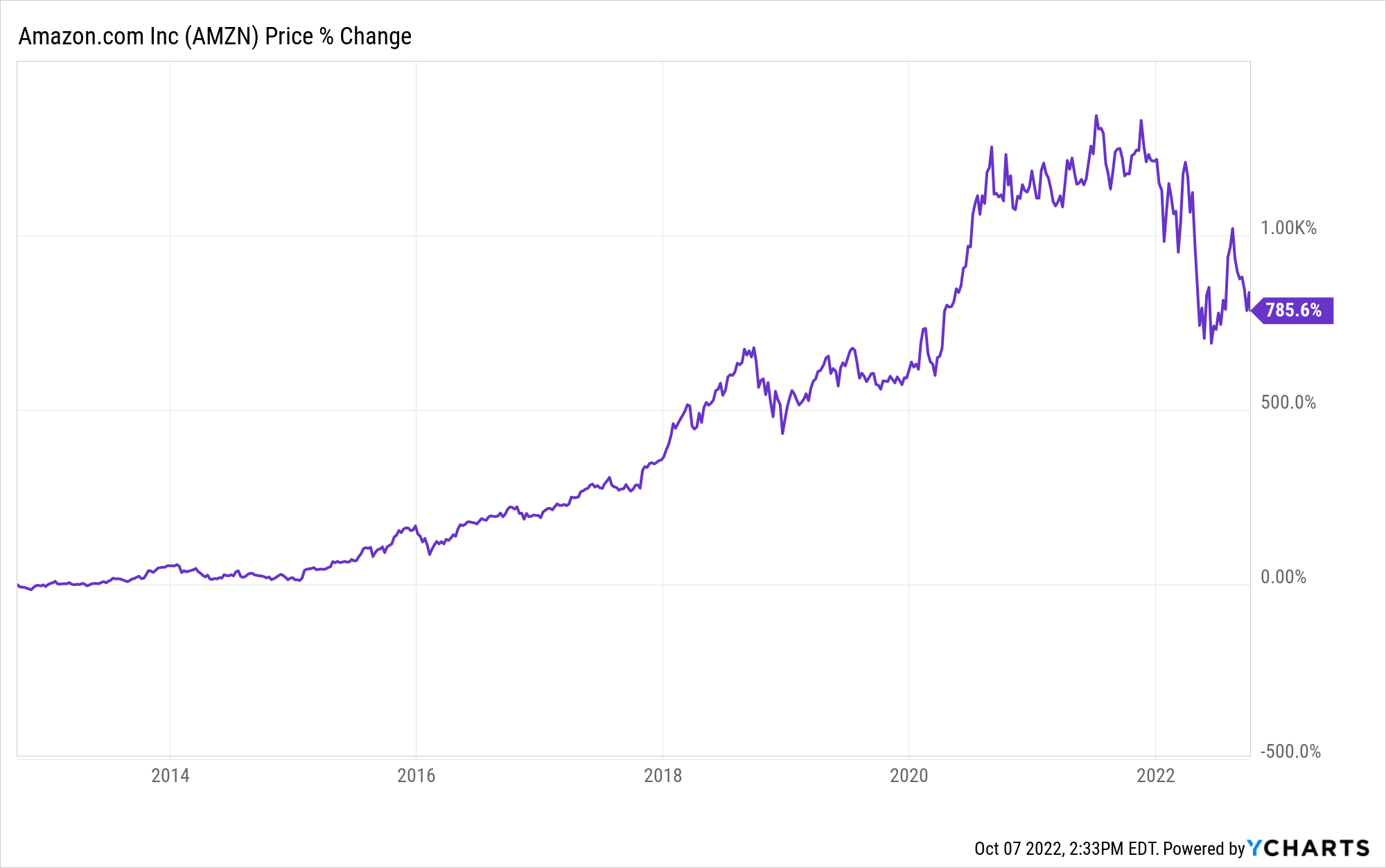

Indeed, buying Opendoor stock today could be like buying Amazon (AMZN) stock back in 1997, before it ruled retail.

Now, with the state of the housing market, you might think that sounds a little bananas.

But from where I sit, Opendoor makes a rather compelling case. In fact, I’ve researched this company top to bottom, inside and out. I see it becoming the “Amazon of houses” over the coming decade — and taking over the multi-trillion-dollar housing market.

In that case, Opendoor stock will soar in the 2020s like Amazon stock did in the 2010s.

{kind=link}

I could go on and on about why I think this will happen. Of course, I’ve done my homework here. We’re talking months upon months of research.

But at the end of the day, the bull thesis can be boiled down to a few sentences.

The Quick Bull Thesis

The real estate market is stuck in the Stone Age. In a world dominated by direct-to-consumer digital processes, buying and selling home remains an oddly physical process.

It’s filled with excessive profit-taking middlemen that make the process slower, more expensive, and more complex than it should be…

Therefore, there exists a huge opportunity to digitize and streamline the home-shopping process. It can be done directly and digitally, between just two parties — and no one else.

That means the process can become fast, cheap, and easy.

This direct process of buying and selling homes is called iBuying.

It’s relatively new, but the adoption of iBuying is starting to soar in the wake of the COVID-19 pandemic. Consumer hesitancy to online shopping has been all but eliminated. And the technologies underlying iBuying’s efficacy — including streaming quality and data-driven pricing algorithms — have dramatically improved.

We see iBuying today where e-commerce was in the late 1990s — in the early stages of enormous, disruptive growth.

And in the iBuying world, Opendoor reigns supreme, without much competition. The company is the biggest iBuyer and operates in the most markets with the most cash. And it has the most talented team and the best technologies, including the best consumer UX and pricing algorithms.

How do I know this? Well, because I personally sold my home to Opendoor. And it was as easy as selling an item on eBay (EBAY).

A Falling Knife in a Down Market?

This year, OPEN has been a falling knife. It’s down more than 87% year-to-date.

Indeed, last week, after the iBuying giant reported third-quarter numbers and Q4 guidance that reflected a dour housing market, OPEN stock crashed. The number of homes Opendoor sold in the third quarter, the prices of those homes, and the profit margins the company netted on those homes all dropped. It’s an ugly market, and Opendoor is caught right in the middle of it.

But if there is one thing we know about the housing market, it is that it always bounces back. Our core thesis remains that the home-shopping process will become increasingly digitized over the next few years and that Opendoor will be the company that pioneers that digitization process.

Therefore, if Opendoor can survive this rough housing market and make it to 2023 without going bankrupt, we think this company will become a titan, and its stock price will soar. And given EBITDA losses are only running about $200- to $300 million a quarter – while the company has $1.5 billion in cash on the balance sheet with over $10 billion in lending capacity – we believe Opendoor will survive.

So long as this housing crash only lasts another few quarters and we get back to normal operating conditions in 2023, Opendoor stock is a fantastic buy.

The Final Word on Opendoor Stock

The housing market will bounce back. The home-selling process will become increasingly digitized. Opendoor won’t go bankrupt. The company has a massive first-mover advantage in creating the marketplace for digitally buying and selling homes. And the stock is ridiculously undervalued at 0.1X sales. Yes, OPEN has been a falling knife and a huge loser – but it’s a winning company with a winning technology platform. And in our opinion, the stock will soon stage a generational comeback.

So… if you missed out on Amazon… here’s your chance to scoop up Amazon 2.0.

Our conviction on Opendoor stock is so high that we made it one of our Top 10 stocks in our flagship investment research advisory, Innovation Investor.

And in that portfolio of world-changers, we’ve identified our highest-conviction long-term picks.

Opendoor is one of those stocks.

But it’s only one of the stocks in our portfolio. So, what are the others?

I’ll give you a hint. It’s a tech startup at the epicenter of the multi-trillion-dollar self-driving revolution. And long-term, it could soar even more than Opendoor.

If buying Opendoor stock today is like buying Amazon stock back in 1997, then buying this stock today is like buying Tesla (TSLA) back in 2013.

What’s the name?

Get the full list – and a whole lot more.

On the date of publication, Luke Lango did not have (either directly or indirectly) any positions in the securities mentioned in this article.